Costing Methods

来源:互联网 发布:MySQL删除重复记录 编辑:程序博客网 时间:2024/04/30 13:50

Standard Costing

Standard costing uses predefined costs that are fixed for a specified period of time. Standard Costing enables you to:

• Control and measure performance.

• Define component costs (material costs) using the projected average acquisition costs and associated indirect costs (material overhead) over the specified period of time.

• Roll up assembly costs using bills of material and routings:

- Use bills of material to determine the component cost of an assembly.

- Use routings to apply both internal (resource) and external (outside processing) conversion costs as well as indirect costs (overhead) to assemblies.

Average Costing

In the Average Costing method, the unit cost of an item is the average value of all receipts of that item per unit, to the inventory. Two types of average costing are supported:

• Moving-average costing

This method uses the transaction cost to derive item costs. As you receive items into inventory, you re-weigh the average unit cost with the transaction value. In certain instances, you also re-weigh the average unit cost when you issue from inventory.

Average costing perpetually values inventory using a costing method based on actual costs, holding inventory at a weighted average cost. At any point in time, the average cost of an item is the cumulative value of all transactions divided by the

cumulative transaction quantity for an item.

• Periodic costing

This method values inventory on a periodic basis. The objectives of periodic costing are:

- To capture actual acquisition costs based on supplier invoiced amounts plus other direct procurement charges required by national legislation or company policy

- To capture actual transaction costs using fully absorbed resource and overhead rates

- To average inventory costs over a prescribed period, rather than on a transactional basis

FIFO/LIFO Costing

FIFO (First In, First Out) and LIFO (Last In, First Out) are perpetual costing methods based on actual costs. These methods are also referred to as layer costing.

Layer costing methods are additional costing methods to complement the Standard and Weighted Average costing methods. A perpetual costing method is selected for each inventory organization including Standard costing, Average costing, FIFO costing, or LIFO costing. Inventory balances and values are updated perpetually after costing of each transaction is sequentially completed.

• FIFO costing is based on the assumption that the first inventory units acquired are the first units used.

• LIFO costing is based on the assumption that the last inventory units acquired are the first units used.

Periodic Average Costing

Periodic average costing establishes costs on a per-item and perperiod basis, using the derived cost and final balance as the beginning balance of the next period. You can use periodic average costing to cost one or more organizations on a periodic basis. This cost is based on invoice price, when available. You can match additional invoiced charges, such as freight, customs, or insurance, to the material receipts. For manufactured items, periodic average costing values inventory by including full absorption of resource and overhead costs.

Periodic Incremental LIFO Costing

Periodic Incremental LIFO costing values inventory by assuming that the most recently received item (last in) is the first to be used or sold (first out), but there is no necessary relationship to the physical movement of specific items.

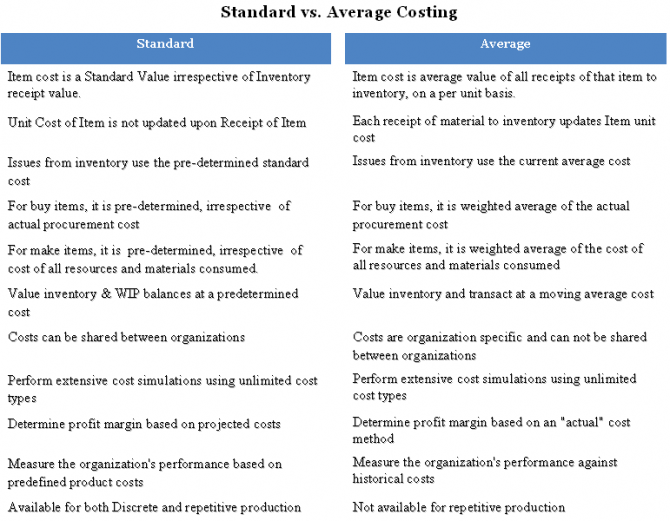

Standard vs Average Costing

refer:http://www.oracleug.com/user-guide/cost-management/standard-costing

refer:http://docs.oracle.com/cd/A60725_05/html/comnls/us/cst/stdavg.htm

- Costing Methods

- Costing variant

- Subcontracting Costing Configuration

- Costing Variants Configuration

- what's "costing alternative"

- 取消的Costing新增

- METHODS

- Methods

- Methods

- 取消的Costing複製功能

- Activity Based Costing configuration in SAP

- 6 guilty pleasures that are costing you

- A new way of real-time product costing

- [科学60s]Climate agreement was costing American workers

- 17.5 Methods

- 17.5 Methods

- Anonymous Methods

- Array.methods

- Uva - 10635 - Prince and Princess(LCS转LIS)

- 使用dbms_metadata.get_ddl出现ORA-31605错误

- 招聘移动开发,老板必问的10个问题

- Linux 的基础命令操作图解

- Android一个工程引用另一个工程

- Costing Methods

- 互联网上的常用端口

- 宁波工程学院[1372] Do What n个数中取出某些数使得和大于T且和最小

- how to view printf output in win32 app on visual studio 2010?

- hdu3343

- 使用Spread.NET创建Y Plot图表

- android应用安全——组件通信安全(Intent)

- jQuery实现ajax

- web开发平台的演变