自回归模型(AR Model)

来源:互联网 发布:linux tail命令详解 编辑:程序博客网 时间:2024/05/16 13:39

转自:http://geodesy.blog.sohu.com/273714573.html

1. 自回归模型的定义

自回归模型(Autoregressive Model)是用自身做回归变量的过程,即利用前期若干时刻的随机变量的线性组合来描述以后某时刻随机变量的线性回归模型[1],它是时间序列中的一种常见形式[2]。

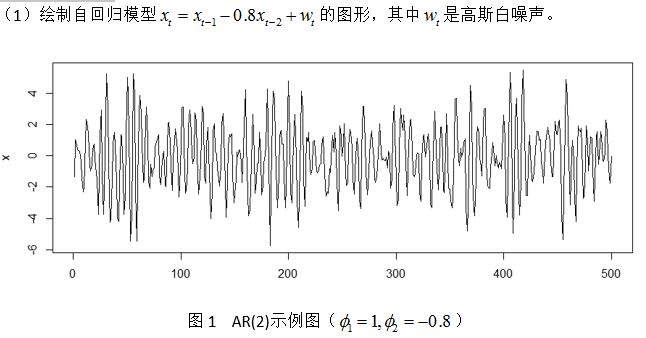

4. AR模型示例

2. AR模型的状态空间形式(AR-Process in State Space Form)

AR模型可以写成状态空间模型的形式[4] [5] [6],令: 3. AR模型的求解

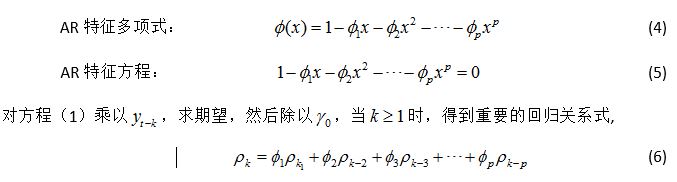

AR模型可以采用Yule-Walker方程的形式进行求解[3]。考虑p阶AR模型有相应的AR特征多项式和相应的AR特征方程:

参考文献

[1]R. H. Shumway and D. S. Stoffer, Time Series Analysis and Its Applications With R Examples, Third ed.: Springer, 2011.

[2]A. V. M. a. P. S. P. Cowpertwait, Introductory Time Series with R: Springer, 2009.

[3]J. D. Cryer and K. S. Chan, Time Series Analysis with With Applications in R(Second Edition): Springer, 2008.

[4]M. Wildi, "An Intro duction to State Space Mo dels," 2013.

[5]J. Durbin and S. J. Koopman, Time Series Analysis by State Space Methods: Second Edition: OUP Oxford, 2012.

[6] J. J. F. Commandeur and S. J. Koopman, An Introduction to State Space Time Series Analysis: OUP Oxford, 2007.

7 0

- 自回归模型(AR Model)

- 时间序列之AR(自回归模型)

- 自回归模型(AR)、移动平均模型(MA)、自回归移动平均模型(ARMA)以及差分自回归移动平均模型(ARIMA)辨析

- 金融时间序列分析:4. AR自回归模型

- 自回归AR模型、移动平均MA模型与自回归移动平均ARMA模型的比较分析

- 基于自回归模型(AR)的自适应阈值的残差比异常检测

- 自回归纹理模型

- 多元线性回归模型(multivariable linear regression model)

- 残差自回归模型

- vofuria的开发(5)替换原vuforia的茶壶模型、改为自己想要的模型AR model

- AR模型

- AR模型

- AR模型

- 模型(Model)类

- Django06模型(Model)

- [转]一阶自回归模型和二阶自回归模型

- Yii AR Model 查询

- Yii AR Model 查询

- 支付宝APP支付接口-PHP

- Wireshark 基本语法,及包过虑规则

- iBET Adidas Yeezy 350 V2 Lucky Draw(Adidas Yeezy 350 V2, ibet newtown casino, Newtown Casino, Newtow

- iOS极速安装CocoaPods详细过程

- 在DOS命令行窗口中显示出用各种字符拼凑出来的各种图案的实现方法,如本人头像

- 自回归模型(AR Model)

- linux 超级用户 切换 为 特定用户

- Eclipse中起始注释和结尾注释的设置,创建注释模版

- react native 遇到的各种问题

- 求最大流Ford-Fulkerson方法(Edmonds-Karp算法)

- resin发布war文件

- SpringMVC从入门到精通(终结版)

- Top N问题(一)基础

- ViewPager懒加载